Car insurance is a legal requirement in the UAE - you cannot register a car, transfer ownership at the RTA or renew your Mulkiya without a valid policy. Yet premiums for the same car and driver can differ by thousands of dirhams between insurers. This 2026 guide explains the types of cover, what insurance really costs, what moves your premium, and how to pay less without leaving yourself exposed.

How car insurance works in the UAE

Every vehicle on UAE roads must carry at least third-party liability cover from an insurer licensed by the Central Bank of the UAE. Policies run for 13 months (12 months of registration plus a one-month grace period), and proof of insurance is checked electronically at registration and renewal. Drive uninsured and you face fines, black points and the risk of paying an accident bill out of pocket - potentially catastrophic if injuries are involved.

Types of cover

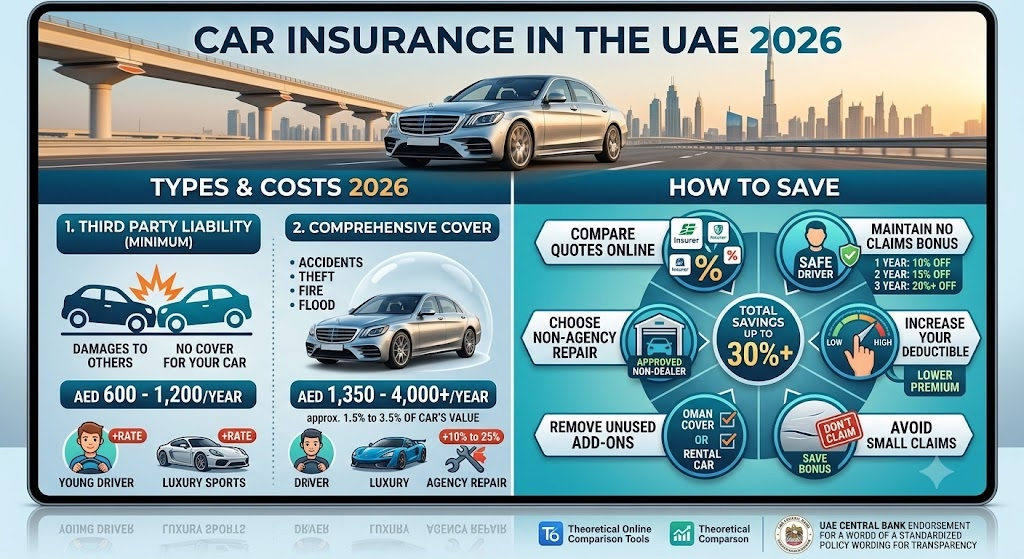

Third-party liability (TPL) - the legal minimum

TPL pays for damage and injury you cause to other people and their property. It pays nothing towards your own car. It is the cheapest option and can make sense for older cars whose market value is low - typically anything worth less than the difference in premium over a few years.

Comprehensive - the sensible default

Comprehensive cover includes TPL and also protects your own car against collision, fire and theft. Depending on the insurer and add-ons, it can extend to natural perils (sandstorms, hail and the flash floods the UAE has seen in recent years), off-road use for 4x4s, personal accident benefits, agency repair, rent-a-car allowance while yours is in the workshop, and GCC-wide or Oman extension cover. If your car is financed, the bank will insist on comprehensive cover - factor it into your budget alongside the repayment when you use the car loan calculator.

Agency vs non-agency repair

Agency repair means accident damage is fixed at the dealer's own workshop with genuine parts - usually offered for the first three to five years of a car's life at a premium of roughly 10-20% more. Non-agency repair uses approved independent garages and keeps the price down. For newer cars still under warranty, agency repair helps protect resale value; for older cars, non-agency is normally the rational choice.

What car insurance costs in 2026

- Comprehensive: typically 1.25%-3% of the insured value per year. A AED 80,000 saloon might cost AED 1,300-2,400; a AED 250,000 SUV could run AED 3,500-7,000+.

- Minimum premiums: regardless of value, insurers apply minimums - roughly AED 1,200-1,300 for saloons and around AED 2,000 for 4x4s on comprehensive.

- Third-party: usually AED 750-1,500 a year depending on engine size, body type and driver profile.

- Electric cars: EV premiums have fallen as repair networks matured, but battery damage clauses vary widely - read them before insuring anything from our electric cars pages.

What moves your premium

- Driver profile - age (under-25s pay loadings), licence age, and nationality-based experience rules at some insurers.

- Claims history - a no-claims certificate earns 10-20% off; multiple claims can double your quote.

- The car itself - value, body type, engine, theft rates for the model, and whether it is GCC-spec or imported. Non-GCC imports often cost noticeably more to insure, and some insurers refuse them.

- Excess (deductible) - the amount you pay per claim; accepting a higher excess lowers the premium.

- Usage and mods - commercial use, off-road cover and performance modifications all raise the price.

Buying and renewing: the process

Get at least three quotes - direct from insurers, via comparison sites, or through your bank - with your Emirates ID, driving licence and Mulkiya to hand. When buying a used car, remember the seller's policy does not transfer: arrange your own cover before the transfer appointment, as our used-car buying guide walks through step by step. Before insuring any used car, run a free VIN check - a hidden accident history can complicate both your premium and any future claim.

Making a claim

After any accident, call the police (999, or use the Dubai Police app for minor incidents) and obtain the police report - insurers will not process a claim without it. Submit the report, your licence, Emirates ID and Mulkiya to the insurer, pay your excess, and the approved garage handles the rest. Green (not-at-fault) reports normally protect your no-claims discount; red (at-fault) reports do not.

Seven ways to pay less in 2026

- Compare at least three quotes every renewal - loyalty is rarely rewarded.

- Carry your no-claims certificate between insurers.

- Choose a sensible higher excess if you can absorb it.

- Skip agency repair once the car is past its warranty years.

- Drop add-ons you do not use (off-road cover for a city car, Oman extension you never claim).

- Insure at realistic market value - over-insuring inflates premium without increasing payout.

- Pick a car that is cheap to insure in the first place: mainstream models from our Toyota and Nissan pages consistently quote lowest, and cars under AED 50,000 usually attract only minimum premiums.

Frequently asked questions

How much does car insurance cost in the UAE?

Comprehensive cover typically costs 1.25%-3% of the car's insured value per year, subject to a minimum premium of roughly AED 1,200-1,300 for saloons and AED 2,000 for 4x4s. Third-party liability cover is cheaper - usually around AED 750-1,500 a year depending on the car and driver. A clean claims history, higher excess and annual payment all bring the price down.

Is third-party or comprehensive insurance better in the UAE?

Third-party liability is the legal minimum and only pays for damage you cause to others - nothing for your own car. Comprehensive also covers your own vehicle for accidents, fire, theft and (if included) natural events like storms and floods. For any car that would be expensive to repair or replace, comprehensive is usually worth the difference; third-party makes sense mainly for older, low-value cars.

Does car insurance transfer to the new owner when buying a used car in the UAE?

No. A car insurance policy covers the policyholder, not the vehicle, so it does not transfer with the car. The buyer must arrange their own insurance before the RTA will complete the ownership transfer - you cannot register a car in your name without a valid policy covering you.

What documents do I need to get car insurance in the UAE?

Typically your Emirates ID, UAE driving licence, and the car's registration card (Mulkiya) - or the vehicle details for a new purchase. Insurers may also ask for a no-claims certificate from your previous insurer to apply a discount, and for modified or imported cars, additional inspection documents.

Insurance is one line in the total cost of ownership - see our UAE car finance guide for the full budget picture, keep an eye on petrol prices, and when you are ready to buy, browse verified used cars and new cars across the UAE. Not ready to own at all? A monthly rental in Dubai bundles insurance into one payment.